Owning a house in Pakistan has become extremely difficult due to rising property prices and rent. That is why the Mera Ghar Mera Ashiana Scheme 2026 is getting massive attention again. The government has relaunched the housing loan program with easier rules, lower markup, and higher loan limits so more families can finally move from rent to ownership.

This updated version is designed for salaried people, small business owners, and overseas Pakistanis who dream of building or buying their first home. The biggest relief is the reduced markup and simplified bank process.

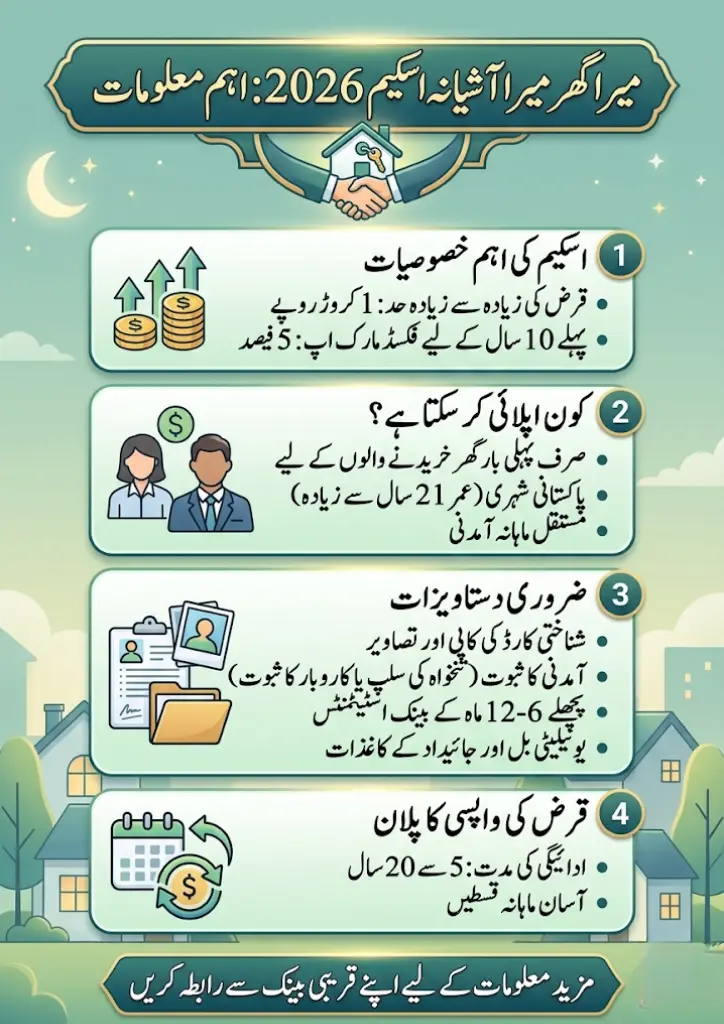

What Changed in Mera Ghar Mera Ashiana Scheme 2026

The latest update made the scheme more realistic and affordable. The maximum loan limit has increased to 1 crore rupees, which means buyers now have more flexibility when choosing a property.

The markup has been fixed at 5% for the first 10 years, which makes monthly installments much easier to manage. Previously, higher interest tiers made repayments stressful for many applicants.

Another major improvement is the wider bank participation. Almost all major banks are now part of the scheme, so applicants have more options and faster processing.

Who Can Apply for Mera Ghar Mera Ashiana Scheme 2026

The scheme mainly targets first-time homeowners. If you already own a house in your name, you will not qualify. The program is designed for people who truly need housing support.

Applicants must be Pakistani citizens with a valid CNIC or NICOP. The minimum age is 21 years. Salaried individuals can apply until retirement age, while business owners can apply until 65.

A steady monthly income is necessary because banks must ensure you can pay installments. Most banks require income between 25,000 and 50,000 rupees or higher depending on the loan amount.

Step-by-Step Guide to Apply Through Banks

The application process is simple, but many people get confused about where to start. Follow these steps carefully.

- First, choose a participating bank near you and request the housing loan application form. Fill it carefully and double-check every detail before submission.

- Next, prepare your documents. Banks will review your financial history to confirm repayment ability. After submission, the bank evaluates your case and verifies the property.

Once approved, the loan is disbursed in stages based on construction or purchase progress. Monthly installments start according to the agreed repayment plan.

Documents You Must Prepare Before Visiting the Bank

Many applications get delayed because of missing documents. Prepare everything in advance to avoid repeated visits.

You need your

- CNIC copy

- passport-size photos

- proof of income

- Salaried people should bring salary slips and job letters, while business owners must provide NTN and business proof.

Bank statements for the last 6–12 months are essential. Utility bills and property documents are also required during property verification.

Loan Repayment Plan Explained Simply

The repayment period ranges from 5 to 20 years. During the first decade, the government subsidy keeps the markup at 5%, which keeps installments manageable.

After ten years, the bank’s standard rate applies. However, by then, a large portion of the loan is usually paid off, reducing long-term pressure.

Common Mistakes Applicants Should Avoid

Many deserving applicants face rejection due to small mistakes. The biggest mistake is applying without stable income proof. Banks prioritize repayment ability.

Incomplete documents and incorrect bank statements also cause delays. Some applicants choose property outside the allowed size range, which leads to rejection.

Always verify eligibility before applying and discuss the loan plan clearly with bank staff.

Expert Tips to Improve Approval Chances

Maintain a clean banking history before applying. Avoid loan defaults or missed payments. A stable job or consistent business income improves approval chances.

Choose a property within your repayment capacity. Smaller loans are approved faster and reduce long-term financial stress.

Final Thoughts on Mera Ghar Mera Ashiana Scheme 2026

The Mera Ghar Mera Ashiana Scheme 2026 is one of the most practical housing opportunities available today. With reduced markup, flexible repayment, and wider bank participation, the dream of home ownership is now more realistic for thousands of families. If you meet the criteria, start preparing your documents and visit a participating bank as soon as possible.

FAQs

- Can overseas Pakistanis apply?

Yes, NICOP holders can apply through participating banks. - Can I buy an old house through the scheme?

Yes, buying or building both are allowed. - Is there an application fee?

Most banks do not charge a processing fee, but legal charges may apply. - What property size is allowed?

Homes between 5 and 10 marla usually qualify. - How long does approval take?

Typically 3–6 weeks depending on documents and bank verification.